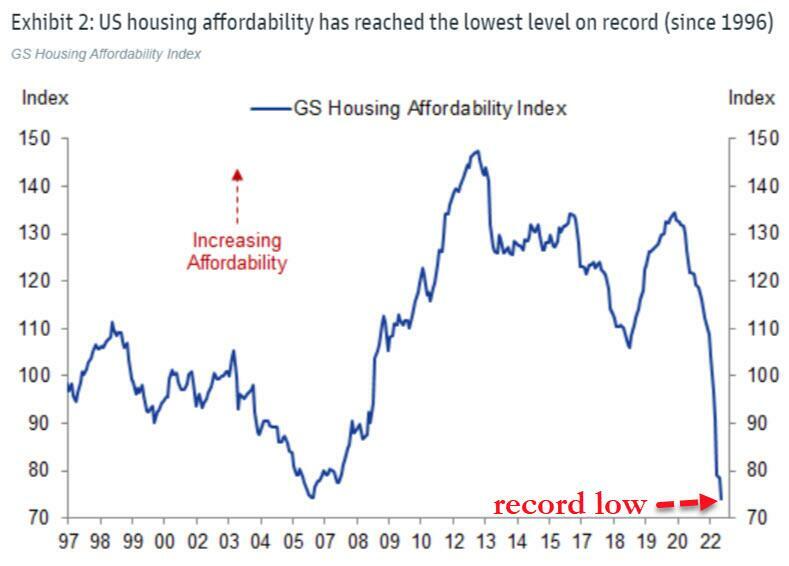

Between cratering homebuilder and homerbuyer confidence…

… record low home affordability…

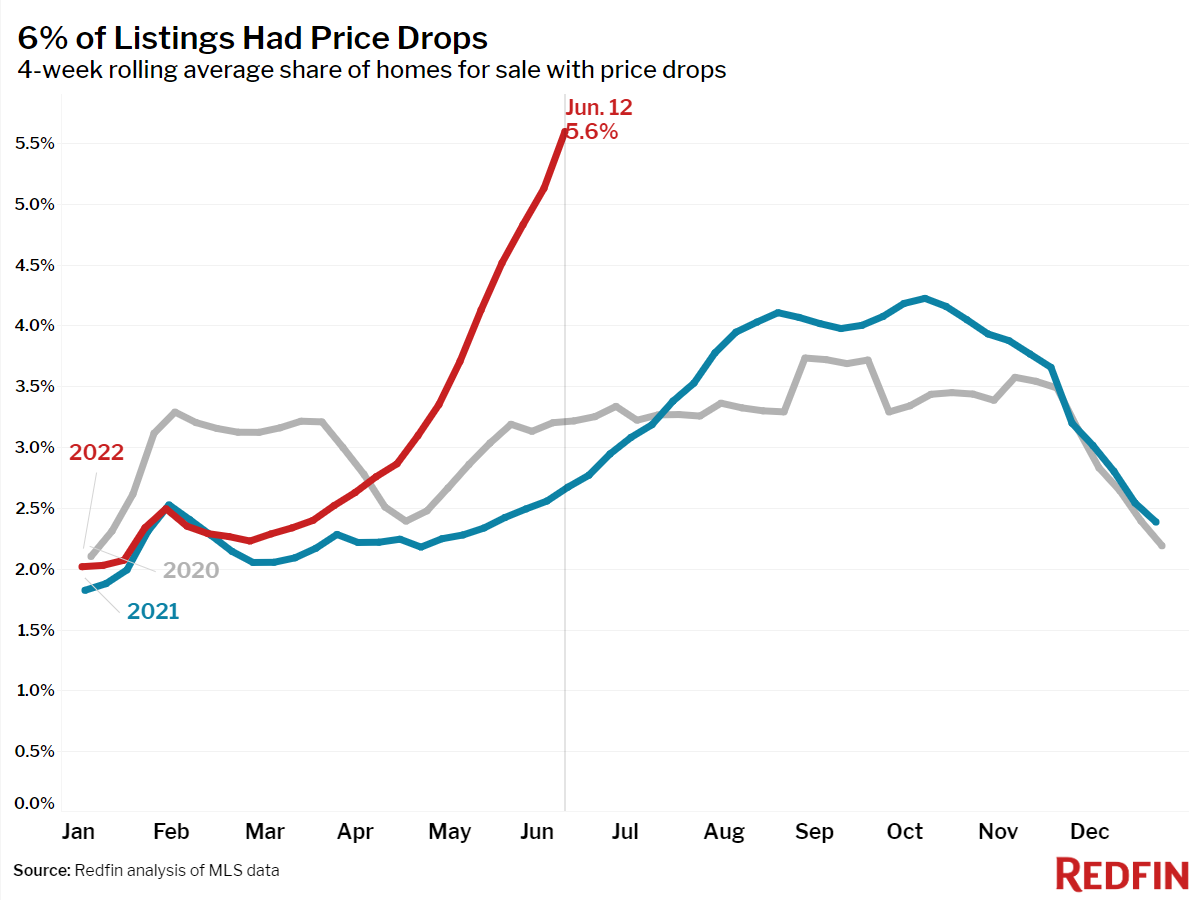

… a record number of new listing with price cuts (amid the collapse in demand).

… plunging housing starts…

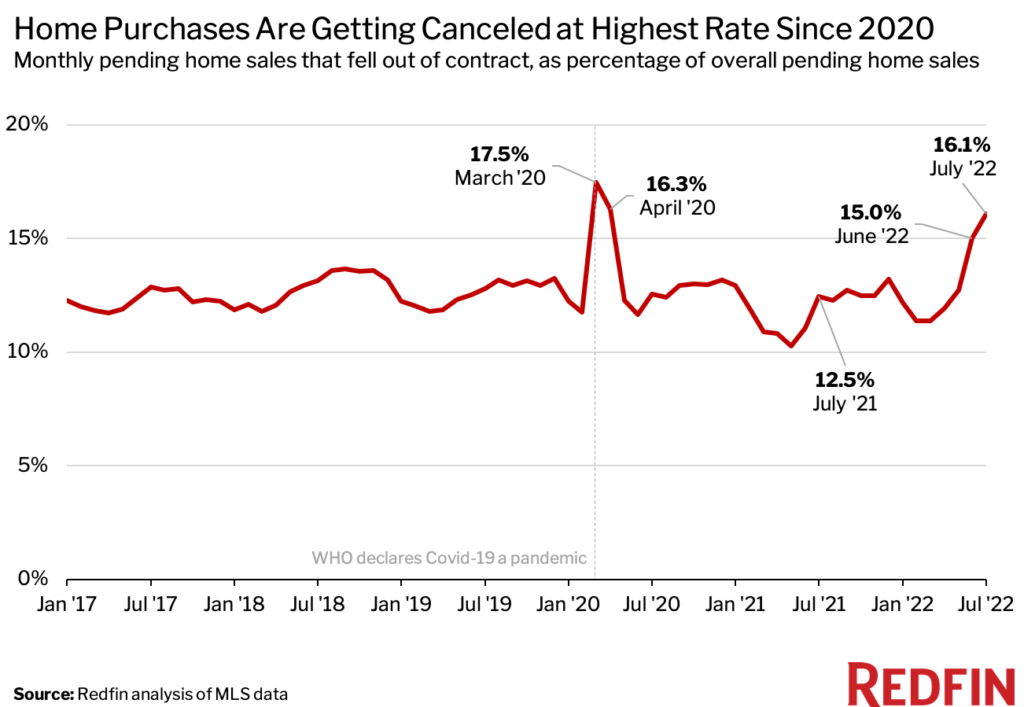

… and so on, as the recent surge in mortgage rates has effectively pushed the housing market into a recession, which is now so widespread that 63,000 home-purchase agreements were called off in July, equal to 16% of homes that went under contract that month. According to Redfin, that’s the highest percentage on record, and only the brief spike during the covid crash – which the promptly reversed – was worse. It’s up from a revised rate of 15% one month earlier and 12.5% one year earlier.

The housing market is slowing as higher mortgage rates sideline many prospective homebuyers. With competition declining, the house hunters who are still in the market are enjoying newfound bargaining power, a striking contrast from just a few months ago, when buyers often had to pull out every stop in order to win. Today’s buyers are more likely to utilize contract contingencies that allow them to back out without financial penalty if something goes wrong. And with an increasing number of homes to choose from, they’re also more likely to call a deal off if a seller refuses to bring the price down or make requested repairs—a situation that has become increasingly common given that sellers are still adjusting to the cooling market.

“Homes are sitting on the market longer now, so buyers realize they have more options and more room to negotiate. They’re asking for repairs, concessions and contingencies, and if sellers say no, they’re backing out and moving on because they’re confident they can find something better,” said Heather Kruayai, a Redfin real estate agent in Jacksonville, FL. “Buyers are also skittish because they’re afraid a potential recession could cause home prices to drop. They don’t want to end up in a situation where they purchase a home and it’s worth $200,000 less in two years, so some are opting to wait in hopes of buying when prices are lower.”

Alexis Malin, another Redfin agent in Jacksonville, warns that there’s no guarantee buyers will be able to find better deals in the future. Annual home-price growth has started to slow—to 8% today from 17% a year ago—but prices are still on the rise and Redfin economists don’t expect them to crash.

“Some buyers who are backing out of deals have this mindset that the market is crashing and they’ll be able to get a home for $100,000 less in six months. That’s not necessarily the case,” she said. “Homes in many parts of Florida are still selling for a pretty penny, so I warn my buyers that the grass might not actually be greener on the other side.”

Some buyers may also be backing out due to 5%-plus mortgage rates. Those who started their search months ago, when rates were closer to 3%, may be realizing the type of home they wanted before is now out of budget since monthly mortgage payments have soared nearly 40% year over year.

“Home-purchase cancellations may begin to taper off as sellers get used to a slower-paced market,” said Redfin Deputy Chief Economist Taylor Marr. “Sellers have already begun to lower their prices after putting their homes on the market. They’ll likely start pricing their properties lower from the get-go and become increasingly open to negotiations.”

And just to confirm how bad the US housing market is, even the morbidly slow rating agency Fitch Ratings said the likelihood of a severe downturn in US housing has increased (although since rating agencies are never allowed to rock the boat, it said that its rating case scenario provides for a more moderate pullback that includes a mid-single-digit decline in housing activity in 2023, and further pressure in 2024.) Fitch also notes that although it recently affirmed the ratings and Stable Outlooks for our US homebuilder portfolio, “ratings could face pressure under a more pronounced downturn scenario that would likely include housing activity falling roughly 30%, or more, over a multi-year period and 10% to 15% declines in home prices.”

* * *

The biggest losers from the latest housing crash aren’t sellers however, but rather homebuilders, who are suddenly finding themselves with a glut of unsold houses.

As Bloomberg notes, with this year’s surge in mortgage rates tossing buyers to the sidelines, the waitlists for new houses are gone and new-home sellers – such as Kevin Brown, who works just south of Houston, are on the front lines of a massive shift. While Brown used to have back-to-back appointments, buyers now just trickle in to his Saratoga Homes sales office. Meanwhile, he’s got 55 houses under construction and five that are complete, all without deals.

“There’s a bit of pressure on us,” Brown said. “Builders have got to hit goals and make their profit, and they don’t like inventory just sitting on the ground.”

An abrupt halt to the pandemic housing boom has left builders that started construction months ago scrambling to adapt. The US supply of new homes relative to sales in June was the highest since the midst of the last crash in 2010. And by early July, buyer traffic to homebuilder websites and sales offices had plunged to the lowest level for the month since 2012, according to a survey of builder sentiment from the National Association of Home Builders.

The new-home pile up underscores a broader shift that’s wreaking havoc in the market. A national housing shortage contributed to years of bidding wars and desperation among buyers who bid up prices to record levels for fear of missing out. But this year’s surge in borrowing costs has now pushed affordability to a breaking point and eased some of the scarcity.

At the same time, the stage is set for longer-term supply constraints as builders pull back. A decade of underbuilding and a bulging population of young people aging into homeownership threatens to prolong the affordability squeeze.

“Despite the fact that there aren’t enough housing units in the country, builders are not willing to take the gamble that’s required to build them,” said Jerry Howard, chief executive officer of the homebuilders group. “They’re afraid that, in a recessionary environment, they won’t be able to sell them.”

In June, 824,000 single-family homes were under construction in the US, more than at any time since October 2006, according to an NAHB analysis of government data. Unsold inventory has ballooned in part because of supply-chain disruptions and labor constraints that created bottlenecks in the production pipeline.

Now, with the economy entering a recession, or already in one, builders are cutting back on starts, trying to avoid having too many completed homes sitting empty. They’re also applying for fewer building permits, which for single-family homes fell in June to a two-year low, according to data from the government.

Not every market is cooling fast. But the change is stark in the pandemic boomtowns where builders piled in to meet demand for out-of-state arrivals, who often bid up prices beyond the reach of locals.

“It has become a very competitive market for builders where they are trying to offload any standing inventory,” said Ali Wolf, chief economist for Zonda, which tracks new-home production. “We may see a period where supply may actually exceed demand for a while in some of the markets that were the most feverish over the past two years.”

Boise, Idaho, is one of those areas where a pandemic bubble is bursting. Remote workers arrived from pricier states such as California, seeking open spaces and fewer virus restrictions. But now Covid restlessness is giving way to fears that the Federal Reserve’s cure for inflation — higher rates — will tip the US into a recession.

Idaho’s biggest builder, CBH Homes, has had about a third of buyers cancel contracts in the past few months, nearly twice the level at the start of the year, according to Corey Barton, the company’s president. He’s got 200 unsold finished homes, compared with 75 at the end of last year, and said he’ll probably surpass the 350 he was left with after the last crash 15 years ago. In a sense the inventory was there all along — it was just hidden, he says.

Builders had been deliberately holding back houses, waiting until they were a couple months from completion before releasing them for sale. That’s because they couldn’t build fast enough to meet sky-high demand. By waiting, they could charge the current market price as materials costs climbed.

But now, the market is getting flooded with listings, Barton said. Homes are finishing or are getting listed earlier in the construction process.

Meanwhile, CBH has cut starts by about half. Subcontractors involved in the early stages of construction, digging out basements or pouring foundations are already feeling it, he said.

“The movement from out of state caused a false market,” Barton said. “We have to accept things for the way they are. It’s going to get tough.”

Builders of new homes find themselves in an especially trick spot, because while most traditional sellers can afford to wait or even postpone a sale if conditions deteriorate, builders will have to discount until they find the market-clearing price, said Benjamin Keys, a real estate professor at the University of Pennsylvania’s Wharton School.

“The homebuilders have an understandable incentive to pull back right now and Americans need more affordable housing,” Keys said.

At Saratoga Homes’s Glendale Lakes sales office, marketing director Christina Nuon said she’s making cold calls to agents and hosting happy hour events to boost sales. The company has a menu of incentives to bring down costs for its entry-level buyers, from $12,000 toward closing costs to a subsidized 30-year mortgage rate of just under 4%.

“Buying down rates, it’s kind of going to be our incentive probably from now on out,” Nuon said. “Just because that’s the only way we can help buyers. We can’t reduce the price any lower.”

Brown, the sales consultant, says the incentives have helped put a dent in inventory: “I am trying to find one buyer at a time,” he said, “and not get overwhelmed by what I have coming up.”

He worries that at the end of a potential recession, continued underbuilding will help keep prices elevated.

More From The Real Estate Guys…

- Sign up for The Real Estate Guys™ New Content Notifcations

- Check out all the great free info in our Special Reports library.

- Don’t miss an episode of The Real Estate Guys™ radio show. Subscribe on iTunes or Android or YouTube!

- Stay connected with The Real Estate Guys™ on Facebook, and our Feedback page.

The Real Estate Guys™ radio show and podcast provides real estate investing news, education, training, and resources to help real estate investors succeed.

Subscribe

Broadcasting since 1997 with over 600 episodes on iTunes!

![]()

![]()

![]()

Love the show? Tell the world! When you promote the show, you help us attract more great guests for your listening pleasure!