Low financing costs, excess savings, and a demand for more space during the pandemic fueled a frenzy in the housing market that sent home prices surging.

Homebuyers, however, are now confronting an increasingly unaffordable housing market that’s been plagued by shortages.

And with the Federal Reserve forcing financing costs higher in recent months, housing market activity has cooled off considerably.

“Housing is likely just at the beginning of recession,“ Tom Porcelli, chief U.S. economist at RBC Capital Market, wrote on Monday. “Of course, a large amount of activity was pulled forward during the pandemic and then you layer on top of that the sharp rise in rates (monthly mortgage payments up about +60% over the last year) and housing was sure to fall hard.“

Last week came with a flood of housing market data, and none of it looked good for those in the market.

For starters, affordability is a big problem.

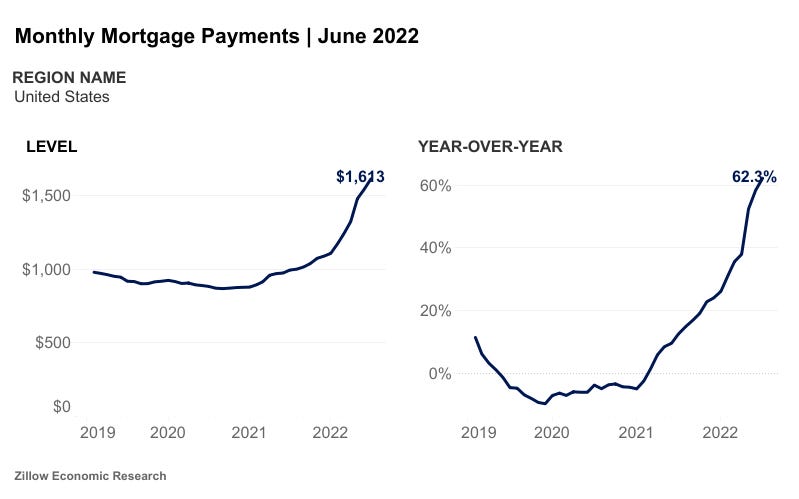

According to Zillow’s monthly housing market report released Tuesday, the monthly mortgage payment on the average U.S. home was $1,613 in June, up 4.5% from a month ago and 62.2% from a year ago.

Again, you can thank cash-flush consumers for helping to fuel a housing market boom that caused home prices to surge over the past two years.

More recently, you have a Fed that’s been tightening financial conditions, which has come with surging mortgage rates. This has made affordability worse.

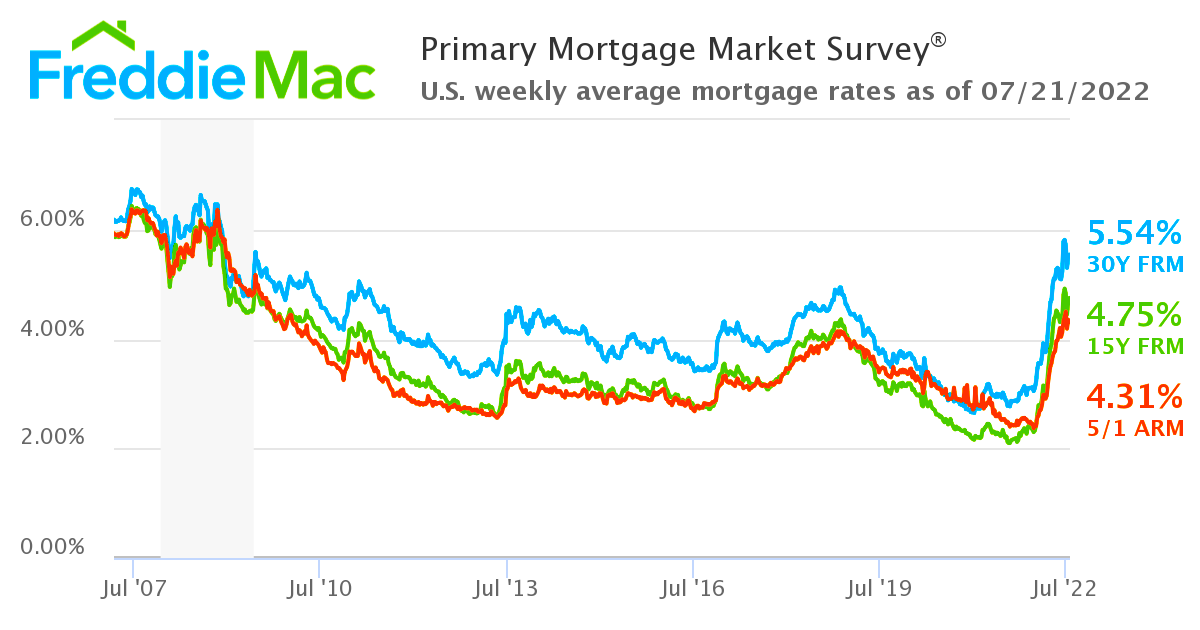

According to Freddie Mac data, the average rate for the 30-year fixed rate mortgage was 5.54% as of July 21. Mortgage rates have surged to levels last seen in December 2008.

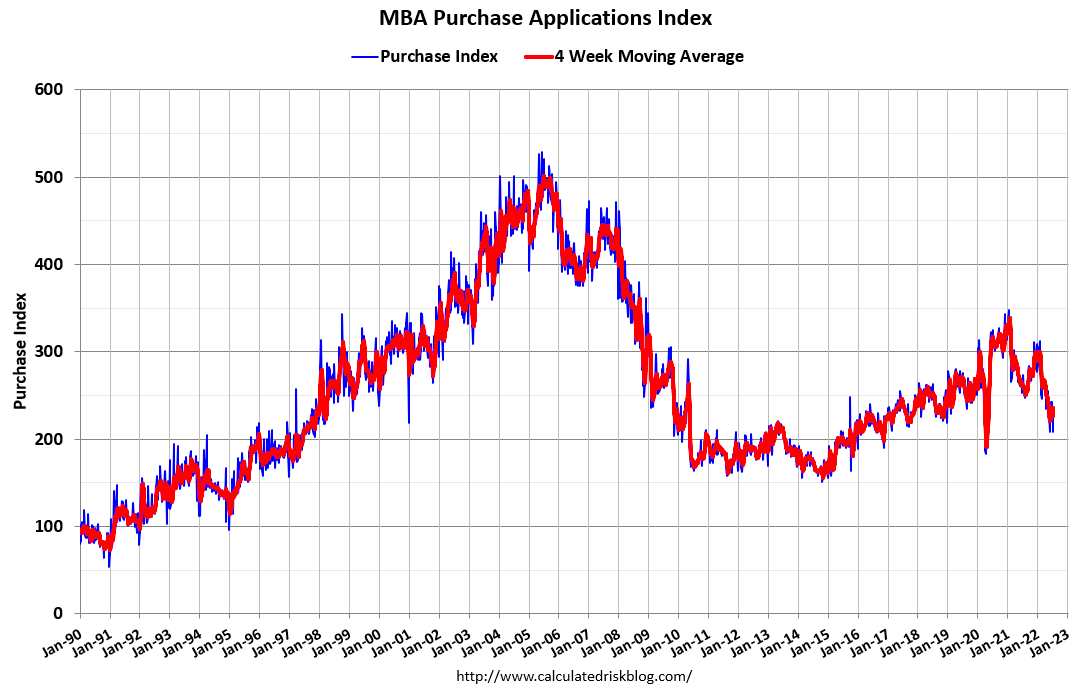

High home prices and high mortgage rates have turned off potential home buyers.

According to the Mortgage Bankers Association (MBA), mortgage purchase and refinance application activity last week fell to its lowest level in 22 years. Bill McBride, author of Calculated Risk, charted the slowdown:

“Purchase activity declined for both conventional and government loans, as the weakening economic outlook, high inflation, and persistent affordability challenges are impacting buyer demand,” the MBA’s Joel Kan said on Wednesday.

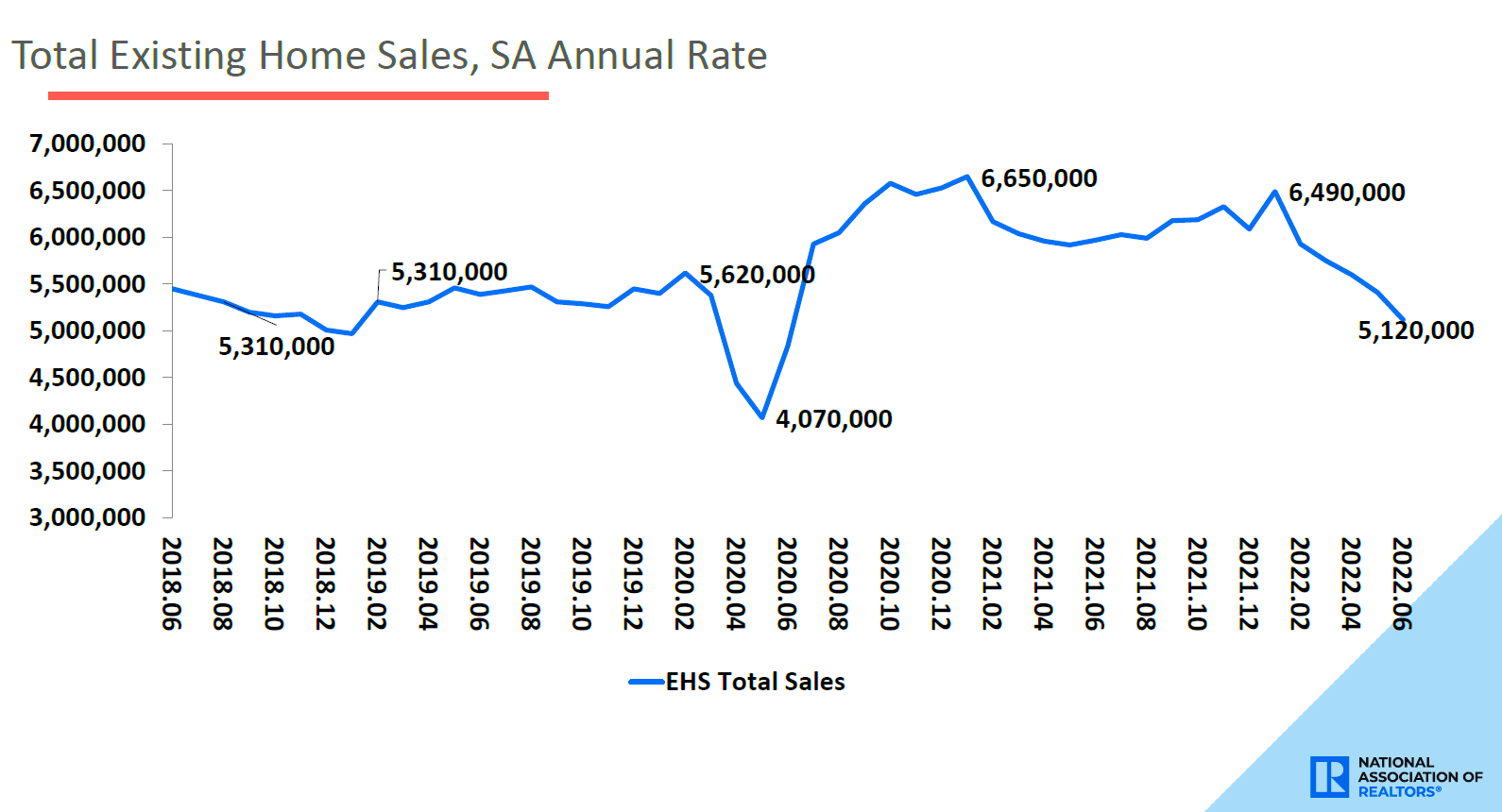

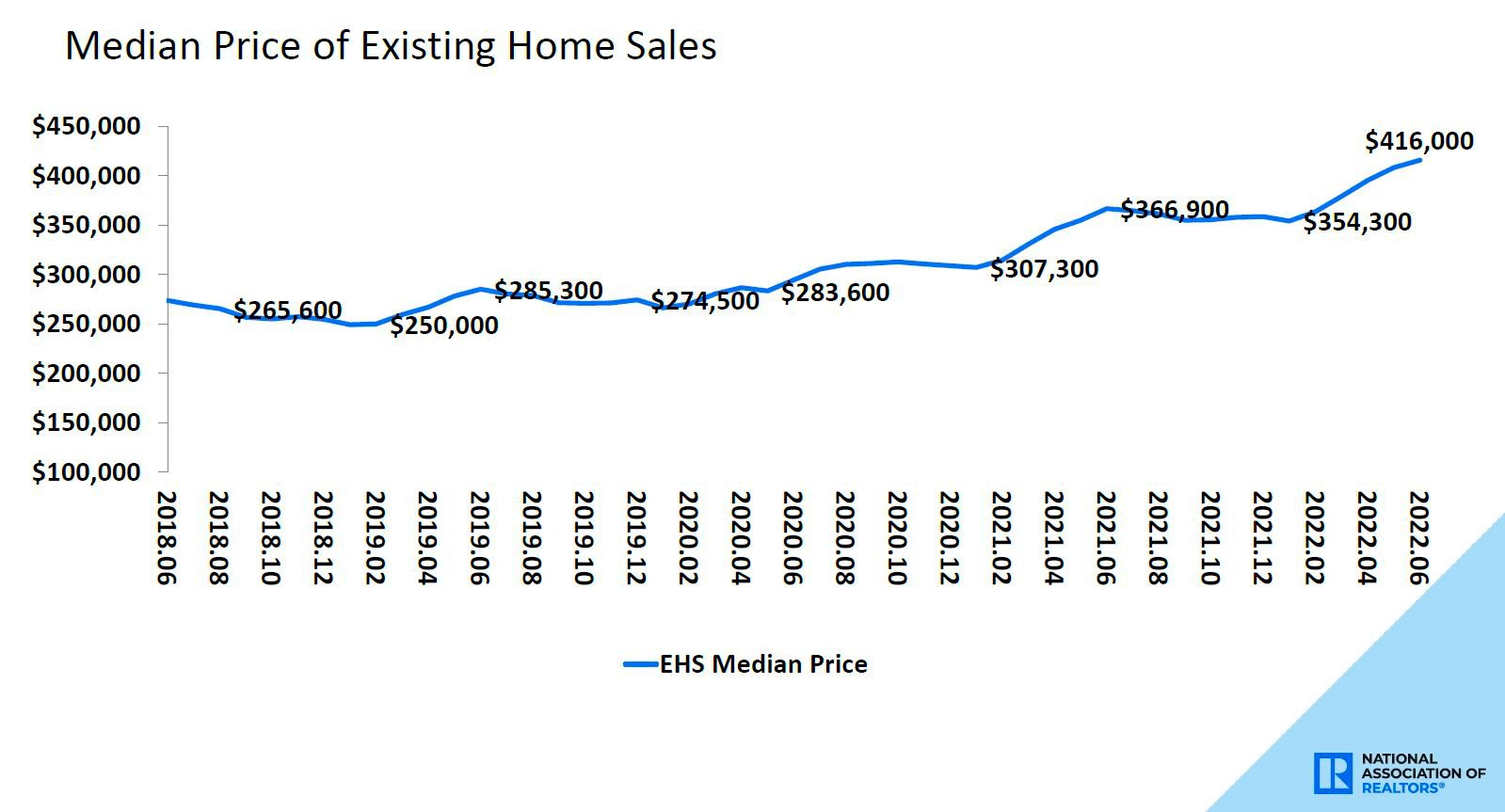

This is all reflected in the declining number of homes being sold.

Sales of previously-owned homes fell 5.4% in June to an annualized rate of 5.12 million units, according to the National Association of Realtors (NAR). It was a 14.2% drop from a year ago.

“Both mortgage rates and home prices have risen too sharply in a short span of time,” NAR chief economist Lawrence Yun said on Wednesday.

Indeed, the price of the average existing home sold was a record $416,000 in June, up 13.4% from a year ago.

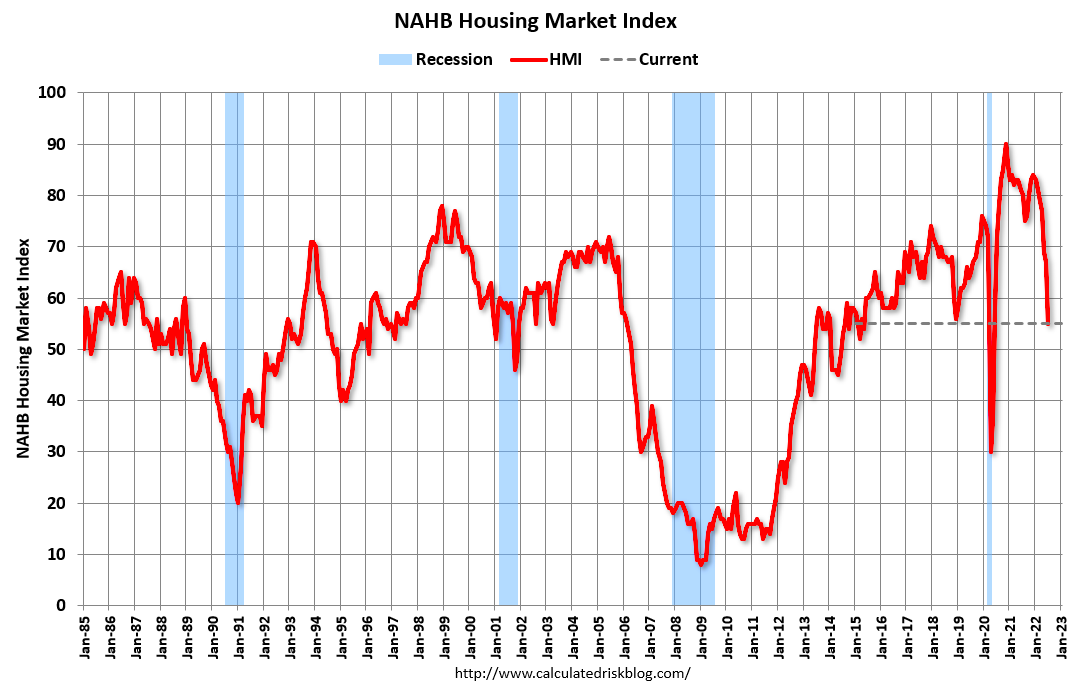

Part of what’s going on in housing is limited supply. But are builders clamoring to take advantage of high selling prices? No.

“Production bottlenecks, rising home building costs and high inflation are causing many builders to halt construction because the cost of land, construction and financing exceeds the market value of the home,” Jerry Konter, Chairman of the National Association of Home Builders (NAHB), said on Monday.

According to NAHB data released Monday, home builder sentiment plunged in July to its lowest level since May 2020.

“Apart from April 2020, this was the largest one-month decline in the 37 year history of the series,” UBS economist Sam Coffin observed. “The housing market index had been trending down gradually since the start of the year, but now, its decline is steeper than at the equivalent time seven months into the housing crisis. In short, it suggests significant further deterioration in homebuilding.“

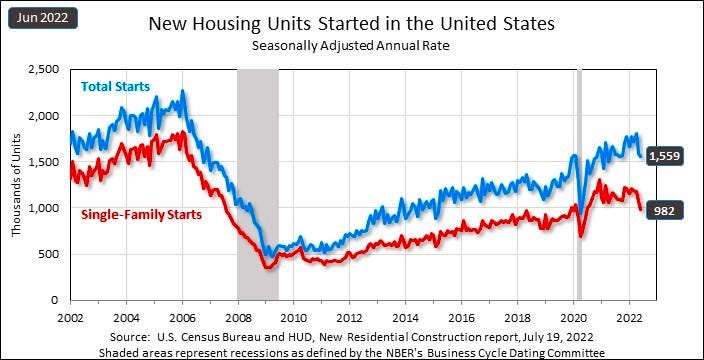

Home construction data confirm the depressed sentiment.

According to Census Bureau data released Tuesday, home construction starts fell to an annualized rate of 1.559 million units in June, down 2.0% from a month ago and down 6.3% from a year ago.

By most measures, housing market activity is cooling and looks ripe to cool further as long as affordability problems persist.

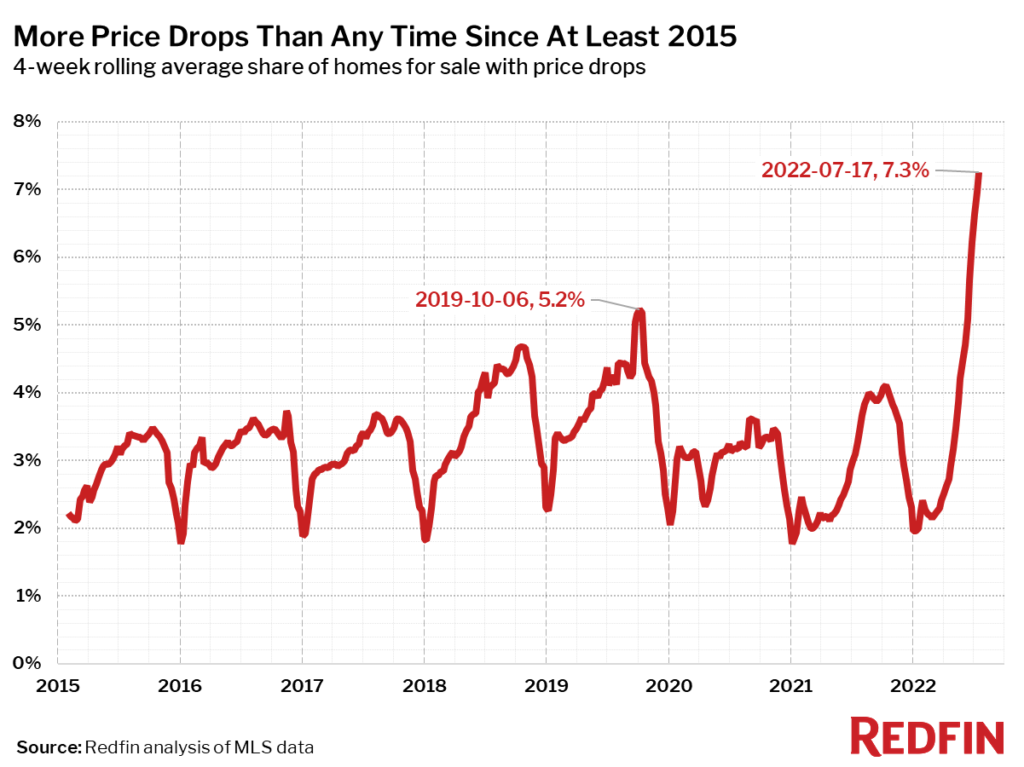

That said, we may soon see prices broadly move lower sooner than later as more and more sellers are finding that they’re listing their homes for too high a price.

“On average, 7.3% of homes for sale each week had a price drop, a record high as far back as the data goes, through the beginning of 2015,” Redfin analyst Tim Ellis wrote.

All that said, what we’re witnessing in the housing market is the desired outcome of the Fed, which continues to use tighter financial conditions — including rising mortgage rates — to cool economic activity in its effort to bring down inflation.

Elsewhere in the economy

Labor market data continues to go from hot to less hot.

Last week, we learned Apple, Google, and Microsoft were among companies slowing their hiring.

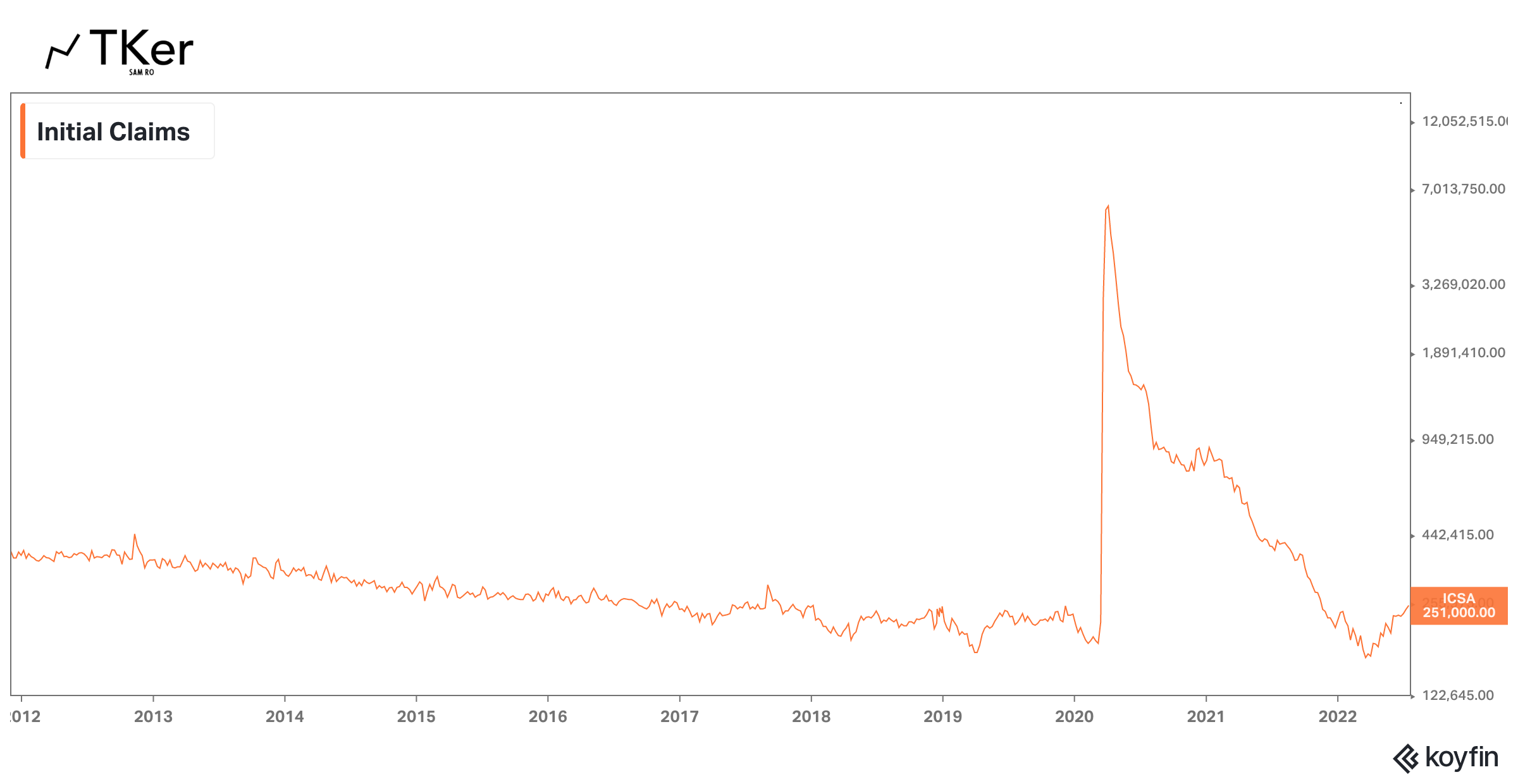

Also, initial claims for unemployment insurance benefits increased to 251,000 during the week ending July 16. It was the fourth consecutive week of increases, and it represented the highest print since November 2021.

While these developments aren’t favorable for job seekers, they’re exactly the kinds of developments the Fed has been hoping for as it battles inflation.

Early signs of contraction

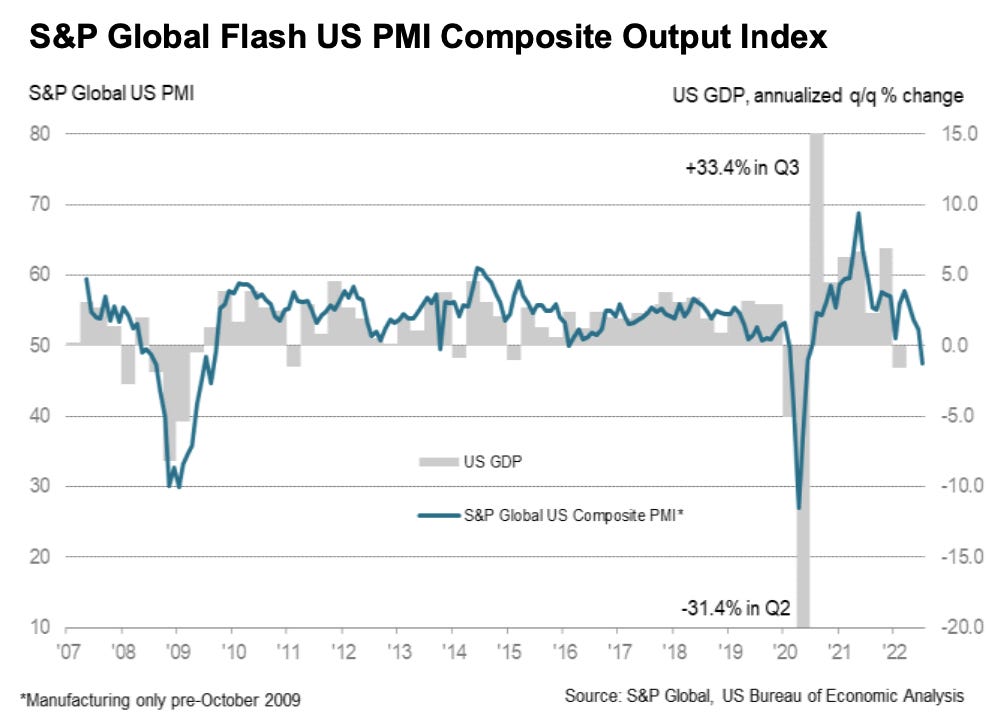

According to S&P Global’s preliminary US Manufacturing PMI report released on Friday, the headline index dropped to 47.5 in July from 52.7 in June. Any reading below 50 signals contraction, and this was the first sub-50 print since June 2020.

The services business activity index fell to 47.0 from 52.7 a month ago. And the manufacturing output index fell to 49.9 from 50.2.

“Excluding pandemic lockdown months, output is falling at a rate not seen since 2009 amid the global financial crisis, with the survey data indicative of GDP falling at an annualized rate of approximately 1%,” Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, said on Friday. “Manufacturing has stalled and the service sector’s rebound from the pandemic has gone into reverse, as the tailwind of pent-up demand has been overcome by the rising cost of living, higher interest rates and growing gloom about the economic outlook.”

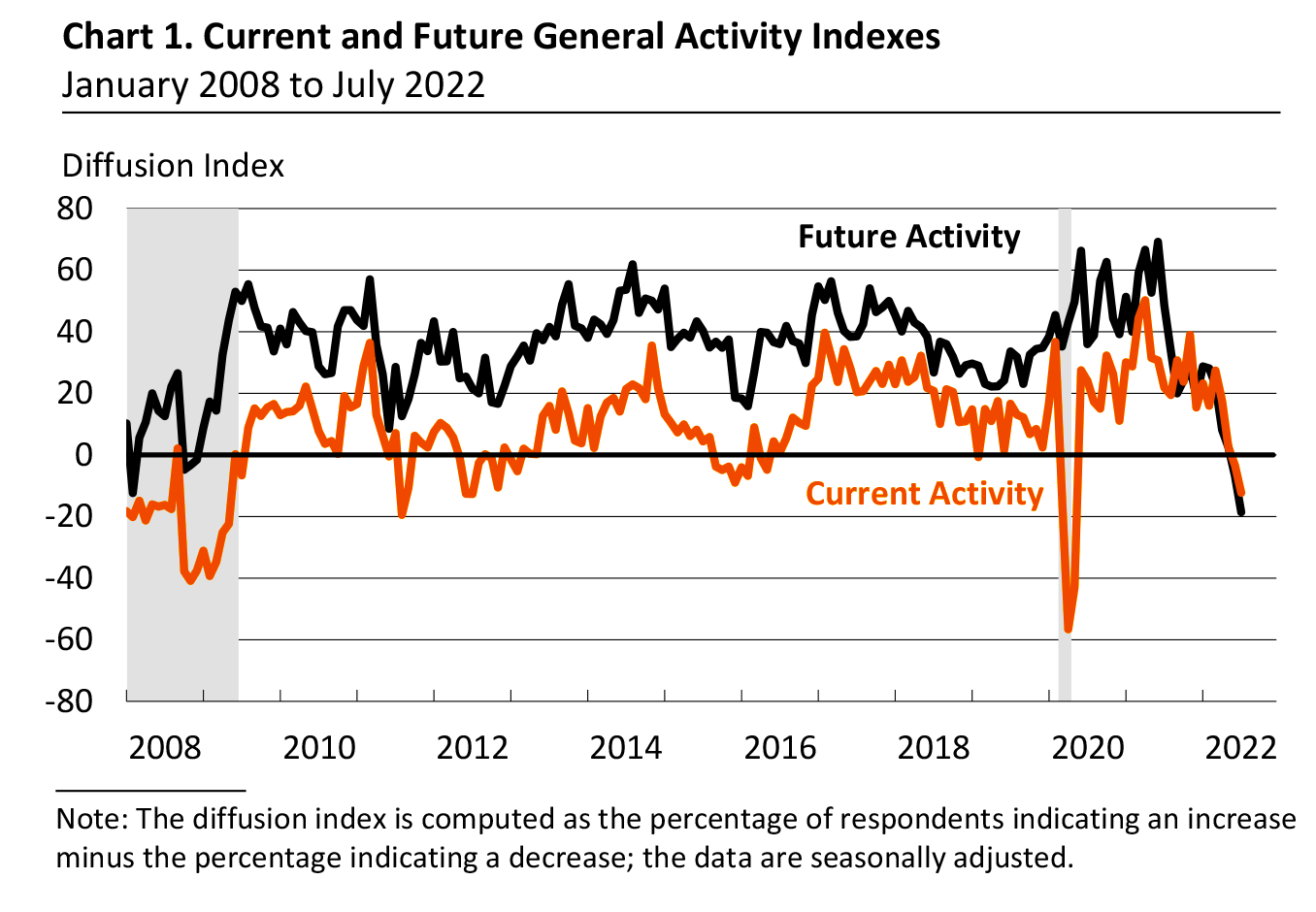

S&P Global’s findings were echoed by the Philly Fed’s Manufacturing Business Outlook Survey released Thursday. The report’s general activity index plunged 9 points to -12.3 in July. Any reading below 0 signals contraction.

The big picture

We continue to live in a world where the Federal Reserve has been trying to slow the economy by bludgeoning financial markets in its efforts to get inflation down.

Indeed, markets have been doing terribly and the economic data has turned decidedly south. And prices for some stuff, including gasoline, have been coming down.

But, it may still be difficult to argue that inflation is moving lower in a “clear and convincing” way, which means we should expect the Fed to remain very hawkish.

The Fed holds its regular monetary policy meeting next Tuesday and Wednesday. At the conclusion, Fed chair Jerome Powell will update us on the central bank’s assessment of inflation and its outlook for monetary policy.

A hawkish or dovish tilt in Powell’s tone could spark volatility in the markets.

More From The Real Estate Guys…

- Sign up for The Real Estate Guys™ New Content Notifcations

- Check out all the great free info in our Special Reports library.

- Don’t miss an episode of The Real Estate Guys™ radio show. Subscribe on iTunes or Android or YouTube!

- Stay connected with The Real Estate Guys™ on Facebook, and our Feedback page.

The Real Estate Guys™ radio show and podcast provides real estate investing news, education, training, and resources to help real estate investors succeed.

Subscribe

Broadcasting since 1997 with over 600 episodes on iTunes!

![]()

![]()

![]()

Love the show? Tell the world! When you promote the show, you help us attract more great guests for your listening pleasure!