As the latest existing home sales report cautioned, with NAR chief economist Larry Yun warning that “housing affordability continues to be a major challenge, as buyers are getting a double whammy: rising mortgage rates and sustained price increases,” BofA joins the chorus warning that last year’s housing euphoria is unlikely to repeat and this year will be a much more challenging year for the housing market given significant headwinds to affordability and ongoing supply-side challenges.

Among the numerous headwinds facing US housing, BofA warns that the Russia/Ukraine conflict adds a new factor to the mix as higher oil and commodity prices will weigh on the consumer’s ability to spend elsewhere, increase uncertainty and recession concerns, and support higher input costs for builders. On the flip side, interest rates may not move much higher and energy-producing areas could see stronger housing demand.

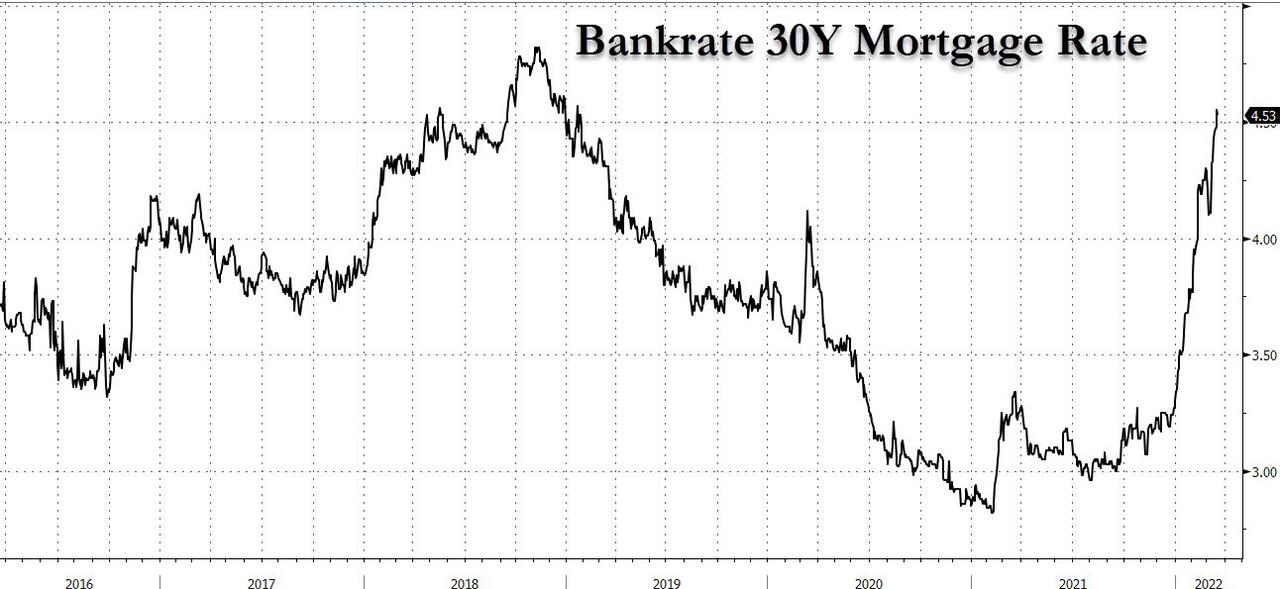

Here are some more details: The pickup in mortgage rates this year has been fast and furious, with the 30yr fixed mortgage rate averaging 4.5% according to Bankrate. This is the highest since 2018 and up more than nearly 100bp from the December average of 3.26%.

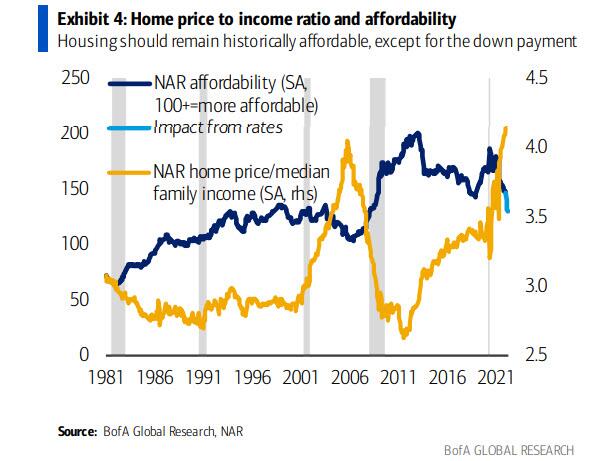

The NAR affordability index provides a way to understand the rates impact to housing demand. Booming home price appreciation last year contributed to diminishing affordability, with the NAR index down 14.7% yoy in December—the latest data point.

The massive rates move this year suggests that the affordability index will see another significant move lower. Paradoxically, further strong home price gains will add to the affordability pullback — BofA currently expects 10% appreciation in Case-Shiller home prices this year, largely due to a continuation of the historical supply demand imbalance.

Supply could further decline as existing homeowners, who account for 40%+ of sales, feel the “lock-in” effect as there is greater disincentive to move and replace their current mortgage that likely has a lower fixed rate, lowering housing turnover.

Housing affordability therefore tends to lead the trajectory for existing home sales, by roughly half a year. According to BofA, the rates shock suggests affordability will be down more than 25% yoy by March – a record decline – with additional downside from higher home prices! If demand follows a similar trajectory, existing home sales could fall below 5mn saar by 2H 2022.

There are likely offsets: BofA lists strong income growth and household balance sheets, favorable demographics, shifting preferences due to remote work, or even a pull forward in demand given expectations of higher rates. However, all that merely justifies the plunge in affordability and the risks are that US consumers get hammered from the coming stagflation; in any case BofA expects overall existing home sales of 5.6mn, pulling back -10% to 2020 levels.

Curiously, despite the upcoming record plunge in housing affordability this year, on a historical basis housing will remain historically affordable (mortgage rates used to be much higher once upon a time, bouncing around 6% during the housing boom era of the early 2000s).

But a major problem is that the barriers to entry are the highest they’ve ever been from the perspective of affording the down payment, which is typically the biggest financial hurdle for first-time homebuyers. As NAR’s Larry Yun put it, “Some who had previously qualified at a 3% mortgage rate are no longer able to buy at the 4% rate.”

Last, and perhaps worst, based on seasonally adjusted NAR data, the median 1-family existing home price to median family income ratio reached a new record high of 4.1 at the end of 2021, surpassing the previous high at the peak of the housing bubble.

The costs and financial hurdles to buying a home are not the only thing that have been on a tear recently. Rents have been on fire over the past year, with the Zillow Observed Rent index soaring 14.9% yoy to $1,904 in January.

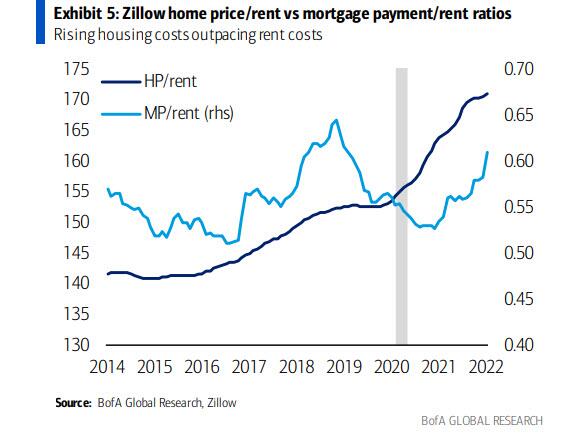

Given housing costs are rising broadly, the question many households face is which is less painful: to buy or to rent? Using Zillow Home Value and Observed Rent Indexes, the home price/rent ratio has worsened dramatically since the pandemic, jumping to 171. And since the hurdle from home prices and affording the down payment is the worst on record, tilting the equation towards renting.

Calculating the implied mortgage based on Zillow home prices and current mortgage rates, BofA finds that the mortgage payment/rent ratio has also been on the rise and is nearly back towards the high of the prior business cycle. That said, the ratio is less than one, suggesting it is still better to buy than rent. This ratio does not account for property taxes or other expenses tied to homeownership, however. When those are included, it’s a toss up whether one should rent or buy…

Consumers appear to understand they are stuck in a lose-lose situation when it comes to buying or renting. If you can afford the historically high down payment, then you will save money on the mortgage compared to paying rent unless mortgage rates spike higher from here.

The Conference Board consumer confidence survey shows that the share of consumers planning to buy a home within 6 months has largely been steady through February. The 3-month average has actually crept up to 6.8% from 6.0% in November, despite much higher mortgage rates. At the same time, consumers have become a lot more humble about the process, highlighting the challenges in the market. The share of respondents who are uncertain about what type of home they plan to buy jumped in 2H 2021 to historically high levels, and the 3-mo average remains at an elevated 3.1% in February reflecting nearly half of total “yes” respondents.

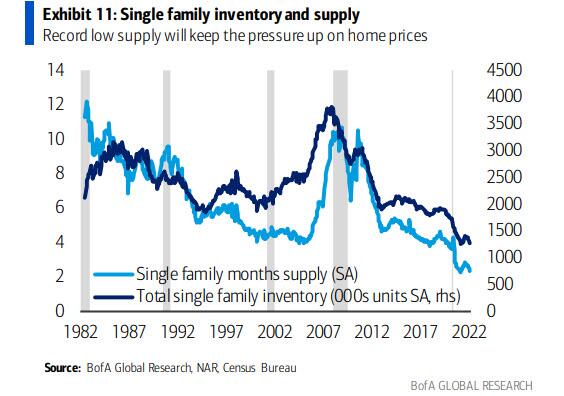

While demand is about to fall off a cliff, especially in a recession/stagflation, a quick look at the supply side also shows an ugly picture: one of the biggest challenges in the housing market has been dwindling supply, which has reached new record lows. Focusing on single-family to see a long history, months supply of new and existing homes dropped to 2.3 in January, down from the 2.6 average in 2021 and nearly half of the 4.1 average in 2019 before the pandemic (see chart below). Strong demand has been part of the equation for lower months supply, with new and existing single family home sales soaring. However, actual inventory levels have also reached historical lows: 1.27mn SA this past January, which is down from 1.33mn last year and 1.86mn in 2019.

At this point, the lack of supply is a well-known problem. Economists are aware, consumers are aware, and builders are aware. However, builders are also facing challenges: lots, labor, lumber has been the catchphrase in recent years, highlighting the three main issues in ramping up new construction, even before the pandemic.

Homebuilders have been impacted by the pandemic-related supply chain chaos, extending build timelines. The number of homes under construction exceeded the number of annualized housing completions for the first time in history in June 2021, and the gap has increased further since then.

Greater multifamily build relative to single family has been a major driver of this development. Single family homes under construction remains below annualized completions, but the gap is closing fast at 142k, not far from the record low of 115k.

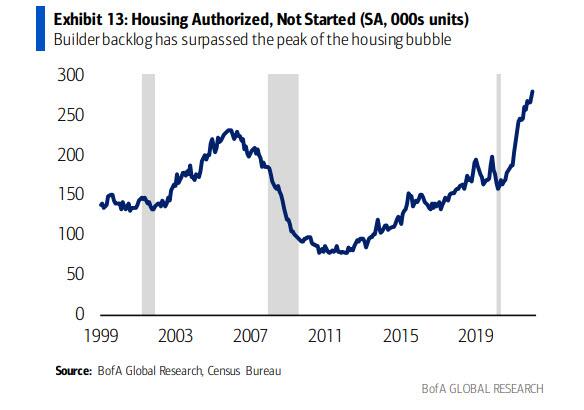

The slower building timelines means an increasing backlog, given robust demand for housing supply. Consistent with this, the number of units authorized but not started reached a record high of 280k. This compares to the peak of 231k during the housing bubble. This backlog underpins the starts and new sales trajectory even if the rates shock causes housing demand to pull back via existing home sales.

Once again, a greater share of multifamily build is the main explanation with single family units authorized but not built of 151k in January below the bubble high of 170k. Still, 151k is considerably above the 2019 average of 89k.

The Russia-Ukraine conflict threatens to add further hiccups, with materials prices being pushed higher. Lumber prices have soared over 47% over the past year and are now only 14% below the all-time peak. Russia is one of the largest lumber exporters in the world, which could pressure prices even higher, as well as a major producer of metals such as aluminum and copper.

Given these extraordinary supply challenges, BofA expects home prices to stay hot at a 10% Y/Yclip in 2022 despite the record plunge in housing affordability and despite existing home sales pulling back. In other words, 2022 will likely be the last hurrah of the US housing market.

More From The Real Estate Guys…

- Check out all the great free info in our Special Reports library.

- Don’t miss an episode of The Real Estate Guys™ radio show. Subscribe on iTunes or Android or YouTube!

- Stay connected with The Real Estate Guys™ on Facebook, and our Feedback page.

The Real Estate Guys™ radio show and podcast provides real estate investing news, education, training, and resources to help real estate investors succeed.

Subscribe

Broadcasting since 1997 with over 600 episodes on iTunes!

![]()

![]()

![]()

Love the show? Tell the world! When you promote the show, you help us attract more great guests for your listening pleasure!