Inflationary concerns are casting doubt on the U.S. economy, but so far are having no impact on the red-hot rental housing market. Rent growth reached another record high in May, as did renter incomes. Leasing activity remained brisk, retention high, and days on market low.

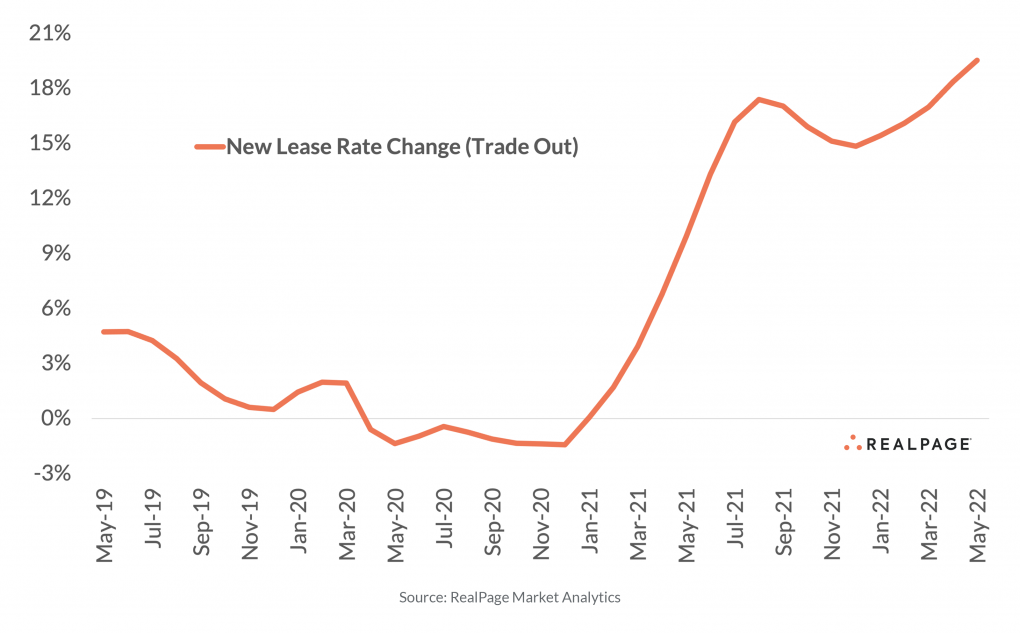

Apartment renters signing new leases in May paid, on average, 19.5% more than previous residents of the same units, based on an analysis of millions of units running on the RealPage platform. The largest increases continued to come in pricier Class A and Class B units – widening the gap with the more affordable Class C apartments.

Renters renewing leases in the same unit continued to see big discounts compared to new renters. That’s particularly true in Class C properties, where affordability concerns tend to be more acute. Class C rents increased 7.9% for renewal leases, compared to an 8.3% year-over-year increase in the overall consumer price index. In other words: For Class C apartment renters, housing costs are climbing less than other expenses.

By comparison, renters in pricier Class A and Class B properties paid around 12% to renew leases in May. Despite the increases, renters usually chose to stay put – with 56.5% signing renewal leases, up 0.5 percentage points year-over-year.

Prospective leasing traffic – an early indicator of demand – appears to be leveling off from the all-time highs set last year. Of course, leveling isn’t the same as cooling. To that point, leasing traffic in May 2022 was still higher than any other May on record prior to 2021.

Beyond the volume of demand, new renters are also bringing higher incomes. Annual household income for new renters signing market-rate leases in May reached a new high approaching $77,000, up 8% year-over-year.

(RealPage will be releasing a detailed study on rental affordability in July at our RealWorld conference in Las Vegas. Unlike other affordability studies, RealPage’s is based on actual leases – both incomes and rents for the same households. The study will break down rent-to-income ratios by asset class and by market, and how they’ve changed over time.)

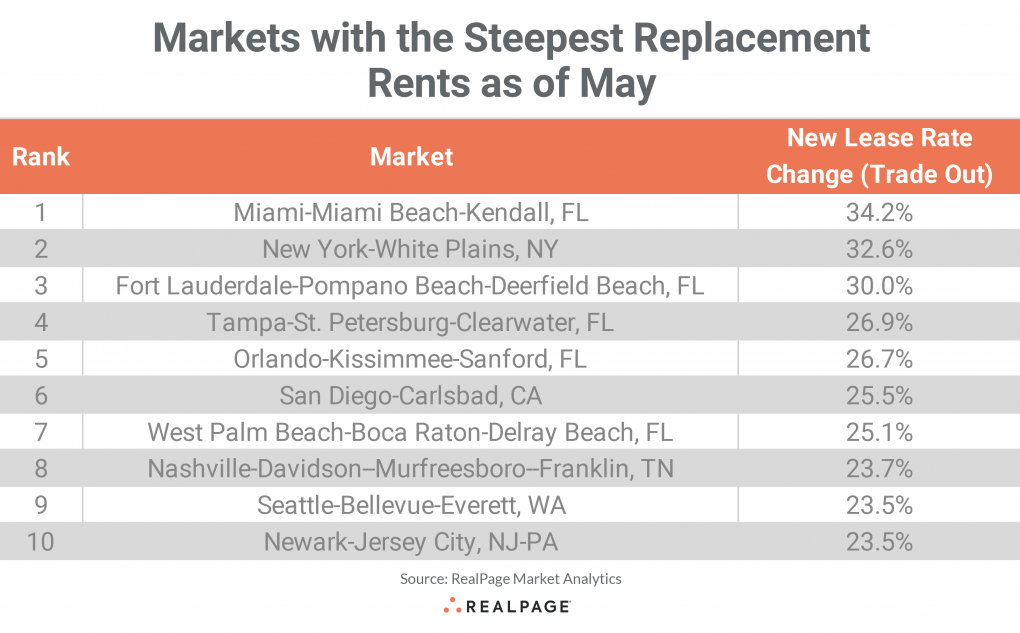

Among individual metro areas, Florida remains home to some of the largest rent increases. All six of Florida’s largest markets posted new lease trade-out (replacement rents for a new renter) of more than 22%, led by Miami at 34.2%.

Rent growth remains sizable across the Sun Belt, and in a few cases have moderated somewhat. Most notably, replacement rents in Phoenix cooled from 26.1% in December to 18.8% in May.

Meanwhile, coastal markets – hit significantly harder with deep rent cuts during the pandemic – are surging up the leaderboard. Replacement rents jumped 32.6% in New York, and by 20% to 26% in San Diego, Seattle, Northern New Jersey, Orange County, San Jose, San Francisco and Boston.

Among top 50-sized metro areas, the smallest increases generally came in the Midwest and the Northeast – although all topped 10% on replacement rents.

More From The Real Estate Guys…

- Check out all the great free info in our Special Reports library.

- Don’t miss an episode of The Real Estate Guys™ radio show. Subscribe on iTunes or Android or YouTube!

- Stay connected with The Real Estate Guys™ on Facebook, and our Feedback page.

The Real Estate Guys™ radio show and podcast provides real estate investing news, education, training, and resources to help real estate investors succeed.

Subscribe

Broadcasting since 1997 with over 600 episodes on iTunes!

![]()

![]()

![]()

Love the show? Tell the world! When you promote the show, you help us attract more great guests for your listening pleasure!