Amid a slew of disappointing US Macro data, preliminary May US PMIs were expected to show slowdowns in btoh manufacturing and services, and the actual prints were worse than expected:

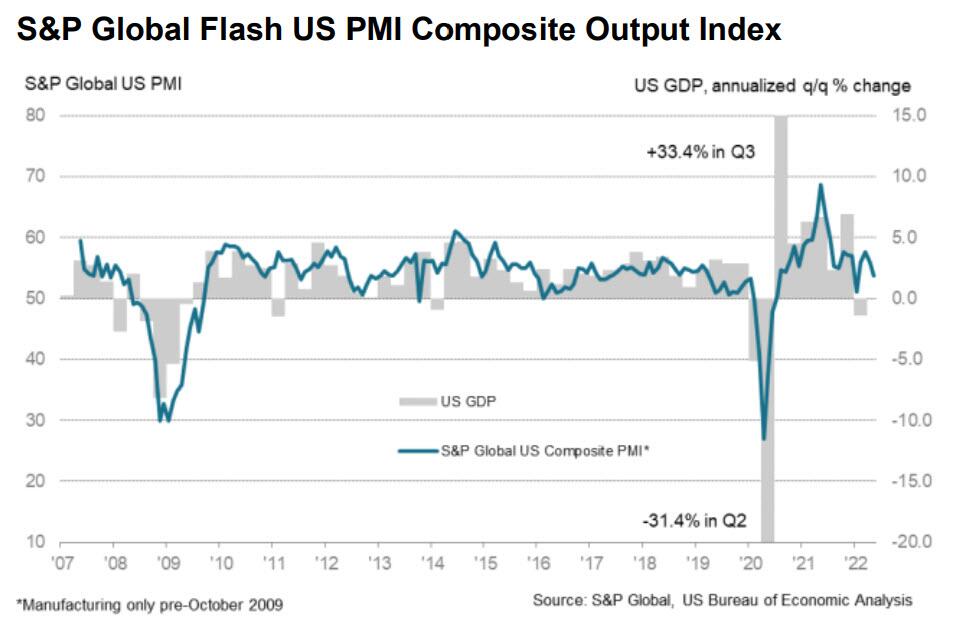

- S&P Global US Manufacturing PMI missed expectations, printing 57.5 (3mo low), below 57.7 expected and down from 59.2 in April

- S&P Global US Services PMI missed expectations, printing 53.5 (4mo low), below 55.2 expected and down from 55.6 in April.

Input prices soared higher again, with the pace of increase edging up to a new series high (since October 2009).

Average prices levied for goods and services also rose markedly, albeit with the rate of inflation easing from April’s series-record high as some companies reported challenges passing further surges in costs on to customers. The pace of increase was the second-fastest on record, however.

This combined drop dragged the composite index down to 4-month lows, but despite all of the headwinds facing businesses, the survey data remain indicative of the economy growing at an annualised rate of 2%, which is also supporting stronger payroll growth. However, as S&P Global notes, “cost pressures have risen to a new survey high which, alongside the encouraging output and employment numbers, will fuel further speculation about the need for further imminent aggressive rate hikes.”

Commenting on the flash PMI data, Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“The early survey data for May indicate that the recent economic growth spurt has lost further momentum. Growth has slowed since peaking in March, most notably in the service sector, as pent up demand following the reopening of the economy after the Omicron wave shows signs of waning. Companies report that demand is coming under pressure from concerns over the cost of living, higher interest rates and a broader economic slowdown.

“Manufacturers in particular also report that capacity continues to be constrained by supply shortages, though these bottlenecks showed further encouraging signs of easing.

All indications remain above 50 and thus signals ‘growth’, therefore offering no respite for a hawkish Fed. Slowing growth but soaring prices – Stagflation, anyone?

More From The Real Estate Guys…

- Check out all the great free info in our Special Reports library.

- Don’t miss an episode of The Real Estate Guys™ radio show. Subscribe on iTunes or Android or YouTube!

- Stay connected with The Real Estate Guys™ on Facebook, and our Feedback page.

The Real Estate Guys™ radio show and podcast provides real estate investing news, education, training, and resources to help real estate investors succeed.

Subscribe

Broadcasting since 1997 with over 600 episodes on iTunes!

![]()

![]()

![]()

Love the show? Tell the world! When you promote the show, you help us attract more great guests for your listening pleasure!