A surge in mortgage rates in early November caused sales and prices to slow, but there are early signs that demand may be creeping back as rates reverse course.

Home sales fell 35.1% year over year in November on a seasonally-adjusted basis—the largest decline in Redfin’s records that date back to 2012. Home-price growth also lost momentum. The median U.S. home-sale price rose just 2.6% from a year earlier, the smallest gain since May 2020, when the onset of the coronavirus pandemic brought the housing market to a near halt.

The housing market continued to cool in November as elevated housing costs kept buyers and sellers on the sidelines. New listings slumped 28.4% year over year, the biggest drop on record aside from April 2020. Despite the decrease in listings, overall supply rose 4.6% from a year earlier—a sign that homes lingered on the market as demand ebbed. Indeed, the typical for-sale home took 37 days to go under contract, up from 23 days a year earlier.

But there are early signs that demand may be starting to creep back as mortgage rates fall. There was a slight downtick in the portion of home-purchase agreements that were canceled in November, and mortgage applications and Redfin’s Homebuyer Demand Index have both been on the rise. Still, these early indicators haven’t translated into more home sales.

Mortgage rates reversed course in late November, dropping below 6.5% after soaring to the highest level in roughly two decades (7.08%) earlier in the month, but they’re still twice as high as they were a year ago. The recent decline was driven by signs of easing inflation, which this week prompted the Federal Reserve to slow the pace of interest-rate hikes. But the Fed signaled that it has more work to do to quell inflation and isn’t yet finished raising rates.

“The worst of inflation is likely in the rearview mirror,” said Redfin Economics Research Lead Chen Zhao. “We do anticipate that mortgage rates will decline slightly further in 2023 as the Fed’s actions continue to bring inflation down, which should ultimately bring more homebuyers back to the market. Still, we have a ways to go until we reach recovery mode, and we may see sales continue to ebb in the short term.”

Zhao continued: “Prospective buyers in places like San Francisco and Austin, where prices have already fallen from a year ago, should pay close attention to a potential turnaround; it could be the time to take action as demand and competitive offers could pick up in the coming months.”

November Highlights

| November 2022 | Month-Over-Month Change | Year-Over-Year Change | |

| Median sale price | $393,682 | -1.5% | 2.6% |

| Homes sold, seasonally-adjusted | 420,213 | -5.5% | -35.1% |

| Pending home sales, seasonally-adjusted | 388,608 | -2.8% | -35.4% |

| New listings, seasonally-adjusted | 467,945 | -4.3% | -28.4% |

| All homes for sale, seasonally-adjusted | 1,511,555 | 0.6% | 4.6% |

| Months of supply | 2.7 | 0.1 | 1.3 |

| Median days on market | 37 | 2 | 15 |

| Share of for-sale homes with a price drop | 20.8% | -1.8 ppts | 10.8 ppts |

| Share of homes sold above final list price | 26.4% | -2.7 ppts | -18 ppts |

| Average sale-to-final-list-price ratio | 98.5% | -0.4 ppts | -2.2 ppts |

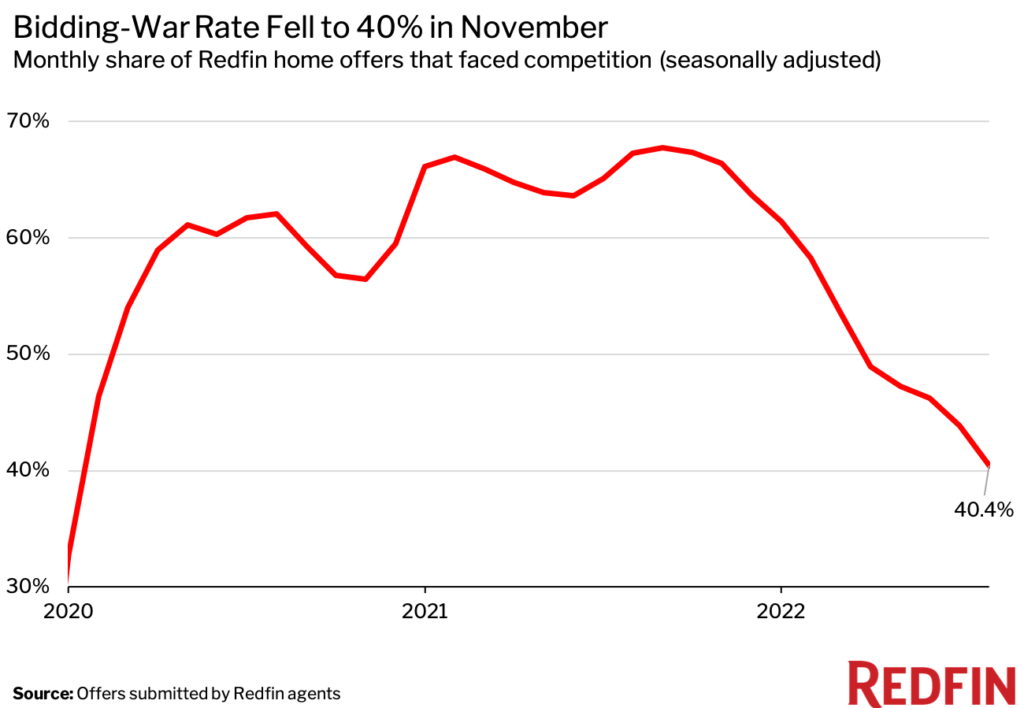

| Share of home offers written by Redfin agents that faced competition (seasonally adjusted) | 40.4% | -3.5 ppts | -26.9 ppts |

| Pending sales that fell out of contract, as % of overall pending sales | 16.8% | -0.4 ppts | 4.7 ppts |

| Average 30-year fixed mortgage rate | 6.81% | -0.09 ppts | 3.74 ppts |

Note: Data is subject to revision

Metro-Level Highlights: Pandemic Boomtowns, Pricey Coastal Cities Drove Market Slowdown

Data in the bullets below came from a list of the 90 U.S. metro areas with populations of at least 750,000, unless otherwise noted. For national and metro-level charts and trends, head to the Redfin Data Center. Refer to our metrics definition page for explanations of metrics used in this report.

- Home sales: Pandemic boomtown Las Vegas saw the biggest drop in home sales, down 51.8% year over year in November. Next came San Jose, CA (-50.1%), Salt Lake City (-49.9%), Stockton, CA (-49.8%) and Oxnard, CA (-48.7%).

- Prices: Eleven metros saw year-over-year declines in median sale prices, with San Francisco leading the drop (-11.1%). It was followed by San Jose, Detroit, Pittsburgh and Boise, ID, all down between 2% and 3%.

- Supply: Pandemic boomtowns North Port, FL and Tampa led the increase in the number of homes for sale, with active listings rising 61.3% and 46.1%, respectively. Next came Nashville, TN (45.1%), New Orleans, LA (40.2%) and Seattle (39.2%). Florida metros likely topped the list because Hurricane Ian drove people to sell their homes; North Port and Cape Coral, another area hit by the storm, were the only two metros where new listings rose on a monthly basis in November.

Scroll down for market-by-market breakdowns on competition and home-purchase cancellations, which can’t be found in the Data Center.

Competition

Data below came from a list of 35 metros—those that had a monthly average of at least 50 offers submitted by Redfin agents from March 2021 to March 2022. An offer is considered part of a bidding war if a Redfin agent reported that it received at least one competing bid. The table is ranked from lowest competition rate to highest.

| Metro Area | Nov. 2022: Share of Redfin Offers That Faced Competition | Oct. 2022: Share of Redfin Offers That Faced Competition | Nov. 2021: Share of Redfin Offers That Faced Competition |

| Orlando, FL | 8.1% | 22.9% | 61.7% |

| Phoenix, AZ | 16.6% | 22.8% | 51.8% |

| Olympia, WA | 16.7% | 42.9% | 79.2% |

| Tampa, FL | 16.7% | 25.0% | 59.3% |

| Riverside, CA | 20.5% | 28.0% | 47.6% |

| Houston, TX | 22.2% | 34.3% | 50.3% |

| Nashville, TN | 22.2% | 10.7% | 61.5% |

| Miami, FL | 23.1% | 32.4% | 55.2% |

| Las Vegas, NV | 23.7% | 27.8% | 57.4% |

| Seattle, WA | 24.5% | 32.1% | 66.0% |

| Denver, CO | 26.4% | 27.0% | 56.2% |

| Raleigh, NC | 28.6% | 28.1% | 68.3% |

| Detroit, MI | 29.6% | 46.2% | 59.3% |

| Dallas, TX | 30.1% | 34.5% | 72.7% |

| Charlotte, NC | 31.4% | 23.8% | 66.1% |

| Austin, TX | 32.1% | 34.1% | 57.2% |

| Indianapolis, IN | 33.3% | 47.1% | 37.2% |

| San Antonio, TX | 33.3% | 27.8% | 51.5% |

| Portland, OR | 34.9% | 36.6% | 60.1% |

| Chicago, IL | 36.3% | 41.3% | 48.3% |

| San Diego, CA | 37.7% | 48.8% | 74.4% |

| Minneapolis, MN | 38.5% | 50.0% | 66.7% |

| Los Angeles, CA | 39.6% | 44.0% | 71.7% |

| Boston, MA | 40.5% | 59.8% | 65.5% |

| Atlanta, GA | 40.7% | 38.2% | 59.6% |

| Colorado Springs, CO | 41.7% | 11.1% | 65.4% |

| Washington, D.C. | 43.3% | 49.7% | 60.4% |

| Philadelphia, PA | 44.2% | 53.7% | 64.1% |

| Sacramento, CA | 46.5% | 39.6% | 74.6% |

| Baltimore, MD | 47.2% | 42.6% | 57.4% |

| New York, NY | 47.5% | 49.0% | 58.1% |

| San Francisco, CA | 47.8% | 52.9% | 68.3% |

| Worcester, MA | 55.6% | 69.2% | 76.3% |

| San Jose, CA | 58.1% | 54.9% | 77.9% |

| Providence, RI | 62.5% | 61.9% | 51.6% |

Note: Metro-level competition data is not seasonally adjusted.

Home-Purchase Cancellations

Data below came from a list of the 50 most populous metro areas and is ranked from highest percentage of cancellations to lowest. San Antonio is excluded due to insufficient data.

| Metro Area | Nov. 2022: Pending Sales That Fell Out of Contract, as % of Overall Pending Sales | Oct. 2022: Pending Sales That Fell Out of Contract, as % of Overall Pending Sales | Nov. 2021: Pending Sales That Fell Out of Contract, as % of Overall Pending Sales |

| Jacksonville, FL | 26.6% | 30.1% | 19.2% |

| Atlanta, GA | 24.5% | 24.1% | 8.6% |

| Orlando, FL | 23.9% | 24.4% | 20.5% |

| Tampa, FL | 23.8% | 26.4% | 20.4% |

| Houston, TX | 23.1% | 22.8% | 19.1% |

| Dallas, TX | 22.7% | 22.3% | 15.6% |

| Las Vegas, NV | 22.1% | 24.1% | 21.0% |

| Fort Lauderdale, FL | 21.9% | 22.5% | 20.7% |

| Fort Worth, TX | 21.3% | 22.1% | 17.3% |

| Riverside, CA | 20.0% | 20.9% | 15.8% |

| Cleveland, OH | 19.5% | 18.2% | 15.8% |

| Phoenix, AZ | 19.5% | 23.9% | 16.5% |

| Indianapolis, IN | 19.3% | 20.9% | 13.0% |

| Miami, FL | 19.2% | 20.6% | 15.3% |

| Chicago, IL | 19.1% | 17.5% | 15.2% |

| Denver, CO | 18.8% | 20.2% | 7.4% |

| Columbus, OH | 18.6% | 17.8% | 15.1% |

| Sacramento, CA | 18.5% | 16.5% | 12.8% |

| West Palm Beach, FL | 18.2% | 22.1% | 19.4% |

| Los Angeles, CA | 18.2% | 18.2% | 13.4% |

| Nashville, TN | 18.1% | 21.6% | 12.5% |

| Austin, TX | 18.1% | 22.0% | 11.4% |

| Pittsburgh, PA | 18.0% | 17.6% | 15.5% |

| Portland, OR | 17.8% | 17.1% | 13.0% |

| Kansas City, MO | 17.6% | 16.8% | 13.9% |

| San Diego, CA | 17.2% | 19.0% | 11.9% |

| Detroit, MI | 17.1% | 17.4% | 16.5% |

| Cincinnati, OH | 16.3% | 13.4% | 13.8% |

| Virginia Beach, VA | 16.0% | 15.5% | 13.0% |

| St. Louis, MO | 15.8% | 16.2% | 13.8% |

| Philadelphia, PA | 15.6% | 14.3% | 11.8% |

| Anaheim, CA | 15.0% | 18.7% | 11.8% |

| Charlotte, NC | 14.9% | 16.5% | 10.8% |

| Washington, D.C. | 14.3% | 13.5% | 11.1% |

| Baltimore, MD | 14.0% | 14.8% | 13.6% |

| Warren, MI | 13.8% | 14.0% | 13.7% |

| Seattle, WA | 13.7% | 11.3% | 7.6% |

| New Brunswick, NJ | 13.4% | 14.3% | 8.0% |

| Providence, RI | 13.1% | 14.7% | 12.4% |

| Newark, NJ | 12.8% | 12.6% | 2.1% |

| Minneapolis, MN | 12.4% | 12.4% | 10.7% |

| Boston, MA | 12.1% | 12.2% | 10.5% |

| Milwaukee, WI | 11.6% | 12.1% | 9.9% |

| Montgomery County, PA | 9.9% | 9.2% | 9.1% |

| New York, NY | 8.9% | 9.9% | 5.0% |

| Oakland, CA | 8.6% | 11.3% | 6.7% |

| San Jose, CA | 8.4% | 8.3% | 5.6% |

| Nassau County, NY | 7.7% | 8.1% | 3.4% |

| San Francisco, CA | 6.3% | 5.9% | 2.8% |

More From The Real Estate Guys…

- Sign up for The Real Estate Guys™ New Content Notifcations

- Check out all the great free info in our Special Reports library.

- Don’t miss an episode of The Real Estate Guys™ radio show. Subscribe on iTunes or Android or YouTube!

- Stay connected with The Real Estate Guys™ on Facebook, and our Feedback page.

The Real Estate Guys™ radio show and podcast provides real estate investing news, education, training, and resources to help real estate investors succeed.

Subscribe

Broadcasting since 1997 with over 600 episodes on iTunes!

![]()

![]()

![]()

Love the show? Tell the world! When you promote the show, you help us attract more great guests for your listening pleasure!