(Bloomberg) — The Federal Reserve will probably have to inflict much more pain on the economy to get inflation under control.

Growth is already slowing in response to the Fed’s repeated interest rate increases, with the housing market softening, technology companies curbing hiring and unemployment claims edging up.

But with inflation proving persistent at a four-decade high, a growing number of analysts say it will take a recession — and markedly higher joblessness — to ease price pressures significantly. A Bloomberg survey of economists this month put the probability of a downturn over the next 12 months at 47.5%, up from 30% in June.

“We have to curb things domestically to help us get where we want to go on inflation,” said Bank of America chief US economist Michael Gapen, who’s forecast a mild recession starting in the second half of 2022.

After raising rates in June by the most since 1994, Fed Chairman Jerome Powell and his colleagues are expected to approve another 75 basis-point hike this week and signal their intention to keep moving higher in the months ahead. Powell has said that failing to restore price stability would be a “bigger mistake” than pushing the US into a recession.

Fed officials though continue to maintain that they can avoid a recession and execute a soft landing of the economy. They argue that the economy has underlying strengths and have voiced hopes that inflation could ease as quickly as it escalated.

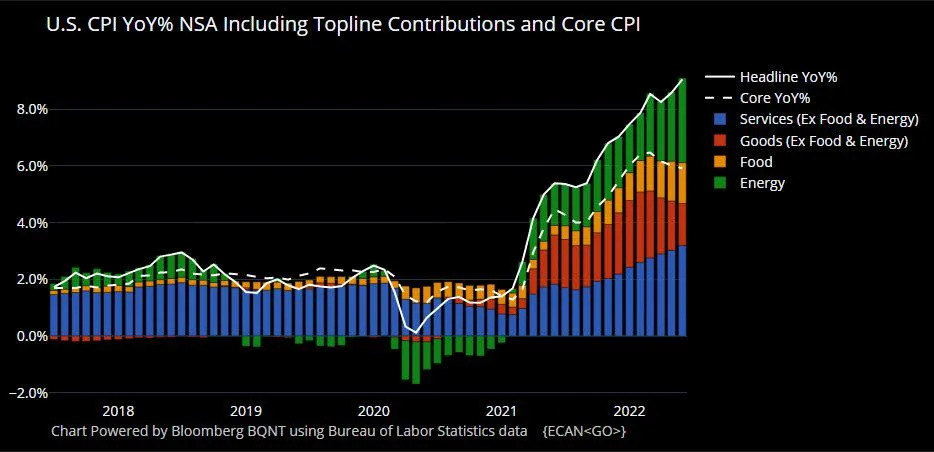

Inflation — as measured by the Fed’s favorite gauge, the personal consumption expenditures price index — was 6.3% in May, well above the central bank’s 2% target.

What Bloomberg Economics Says

“The chance of a downturn in the next 12 months has risen to 38%, significantly higher than zero when we ran the model a month ago. The model sees a 100% probability of recession in the next 24 months.” –– Eliza Winger, Anna Wong and Yelena Shulyatyeva (economists)

The more popular consumer price index is running hotter: It rose 9.1% in June from a year earlier. Three-quarters of the goods and services in the CPI basket increased at an annualized rate in excess of 4% in June from May.

“Inflation is entrenched and spreading,” said former Fed Vice Chair and Brookings Institution senior fellow Donald Kohn.

The central bank faces a tricky job because at least some of the upward pressure on inflation is not from excess demand – which it can control – but from supply disruptions that it is powerless to affect stemming from Russia’s invasion of Ukraine and the pandemic.

An added complication, according to ex-Fed Vice Chair Alan Blinder: Monetary policy impacts inflation with very long lags of perhaps two or three years.

Traders in the federal funds futures market are betting the Fed will raise rates to about 3.5% by year end, from 1.5% to 1.75% now, before beginning to cut them in the latter half of 2023.

Former Treasury Secretary Lawrence Summers doubts that’s how it will play out.

“My instinct is that you’d not see rates cut as soon as people think,” the Harvard University professor and paid Bloomberg Television contributor said.

“The Fed has to be careful. If you look at the history of the 60’s and 70’s, there were moments when monetary policy eased a bit and things didn’t tend to work out so well,” he added, referring to episodes where the Fed loosened credit before stamping out inflation.

Instead of cutting rates, the Fed will likely raise them to 5% or higher next year to try to bring price pressures to heel, Dreyfus and Mellon chief economist Vincent Reinhart said. That will help precipitate a contraction that increases unemployment to about 6%, from 3.6% now, but leaves inflation above 3%, the central bank veteran said.

Policy makers have little choice but to push rates higher because they can’t afford to allow inflation expectations to escalate, ex-Fed Governor Laurence Meyer said. If that happened, the battle to contain inflation would be lost because companies and workers would begin to act in ways that would push prices ever higher.

Meyer, who heads the Monetary Policy Analytics consulting firm, foresees a downturn that reduces gross domestic product by 0.7% next year, raises unemployment to 5% and returns inflation to the Fed’s 2% target in 2024.

“A mild recession is probably pretty good from the Fed’s point of view, given the situation we’re in and how bad it looks,” he said.

Some analysts contend the US is already in a recession. GDP contracted at a 1.6% annualized pace in the first quarter and may have shrunk further in the second, at least according to the Atlanta Fed’s economy tracker. (Economists surveyed by Bloomberg forecast a rebound).

If the Atlanta Fed estimate is borne out by official data on July 28 — the day after the Fed’s rate decision — that would meet the popular definition of a recession: two straight quarters of negative growth.

Fed policy makers have already pushed back on that narrative, pointing to the strength of the job market. “It’s really odd to think of an economy where you add 2.5 million workers and output goes down,” Fed Governor Christopher Waller said on July 7, while stressing his determination to lower inflation to 2%.

Supply Shocks

In a paper presented to a European Central Bank conference last month, researchers found that one-third of US inflation through the end of 2021 was due to supply shocks.

The shocks “are happening in different sectors, at different times, in different countries,” one of the researchers, University of Maryland professor Sebnem Kalemli-Ozcan, said. “This is not in the central banking playbook.”

While the Fed needs to respond to elevated inflation by curbing excess demand, it should be careful not to overdo it, she said.

Hopes for an end to supply chain snarls keep getting frustrated, especially as China struggles with its Covid Zero containment policy. Two-thirds of companies surveyed by the National Association of Manufacturers last quarter don’t expect supply chain disruptions to abate until 2023 or after.

Blinder said he’s feeling slightly better about the possibility of an economic soft landing given recent drops in energy and food prices. But he’s unsure how durable those declines will be and still pegs the chances of a recession above 50%.

“The odds are against the Fed managing this,” the Princeton University professor said.

©2022 Bloomberg L.P.

More From The Real Estate Guys…

- Sign up for The Real Estate Guys™ New Content Notifcations

- Check out all the great free info in our Special Reports library.

- Don’t miss an episode of The Real Estate Guys™ radio show. Subscribe on iTunes or Android or YouTube!

- Stay connected with The Real Estate Guys™ on Facebook, and our Feedback page.

The Real Estate Guys™ radio show and podcast provides real estate investing news, education, training, and resources to help real estate investors succeed.

Subscribe

Broadcasting since 1997 with over 600 episodes on iTunes!

![]()

![]()

![]()

Love the show? Tell the world! When you promote the show, you help us attract more great guests for your listening pleasure!