Most investors don’t really know what it means … or what to do about it …

Real estate investors are more likely to be interested in grading slopes than yield curves. And the Fed’s balance sheet? That’s REALLY esoteric and boring.

BUT … the Fed is the most powerful and influential financial force in the world … affecting the stock and bond markets (where mortgage rates are set), the economy, and even geo-politics.

The Fed seems to prefer hiding in the shadows …

… except when diverting attention from charts like the one below with cryptic congressional testimony and occasional PR appearances on TV.

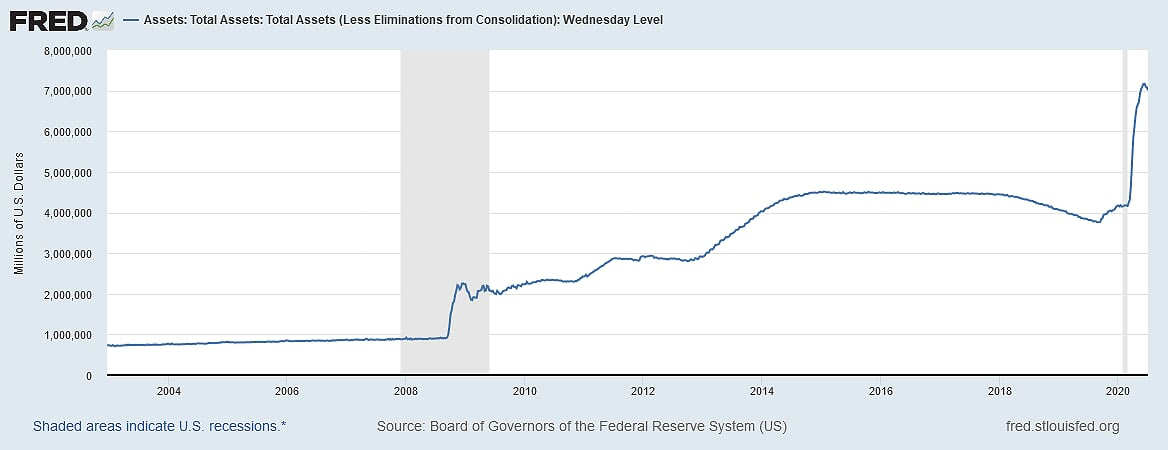

This chart shows the Fed’s ballooning balance sheet …

The numbers might be too small to read, but they’re too big to comprehend … with over $7 trillion of assets (nearly double from just 4 months ago).

You may or may not know what it means, but set that aside right now … and just look at the slow and stable trajectory leading into the end of 2008 …

… and the “big” spike at the beginning of 2009.

Bring back any memories?

We found flipping the chart over helps …

Now, instead of looking like a positive, happy, upward trend … it looks more like the way it felt …

… like you were paddling along on a river until late 2008 when … whoosh! You went into a rough patch of white waters.

Then after a bit of a bumpy ride, you settled into a deep but slow descent into “the eye of the storm” (yes, we just mixed the metaphor) where it seemed stable and trending up.

Then some headwind … you might say your momentum was tapering … and then a little teaser turbulence right before …

WHOOSH!!! Over the waterfall.

This is what it FEELS like for investors riding waves of Fed liquidity via “quantitative easing” (Fedspeak for printing unfathomable amounts of dollars).

Of course, the Fed doesn’t really “print” … that’s so 20th century.

Here’s the official explanation straight from Fed Chairman Jerome Powell’s appearance on 60 minutes:

60 MINUTES: Fair to say you simply flooded the system with money?

POWELL: Yes. We did. That’s another way to think about it. We did.

*** (ANOTHER way to think about it? What’s the first way???) ***

60 MINUTES: Where does it come from? Do you just print it?

POWELL: We print it digitally. So as a central bank, we have the ability to create money digitally. And we do that by buying Treasury Bills or bonds or other government guaranteed securities. And that actually increases the money supply.

Hopefully, that’s VERY clear.

The Fed, by their own admission, simply conjures dollars out of thin air and uses them to buy government-backed debt.

Keep this in mind when you’re perplexed about why the government not only grows its own debt but seems all too willing to guarantee private debt also.

But don’t think about all that too much now. Let’s focus on the discussion at hand …

The Fed’s balance sheet shows HOW MUCH digital money the Fed conjures out of thin air … as reflected by how much government-backed debt they own.

Think about this …

The Fed creates dollars out of thin air at no cost. At this point, it has no value because it cost nothing to create.

Those fresh dollars only become valuable later when someone who did real work and produced a real product or service is willing to trade their product for those previously worthless dollars.

Doesn’t seem quite fair to the person doing real work. But that’s a rant for another day.

Of course, the Fed doesn’t actually put the money directly into circulation. They loan it to the government, who then must spend it into circulation.

Seems like a pretty good deal for the government. They get to spend lots of money to buy nice things … like votes.

If we didn’t know better, we’d be tempted to think the Fed and Uncle Sam have a bit of a racket going.

Nah.

So if the Fed prints dollars for free and then loans them to the government, wouldn’t this make them separate parties?

Good catch. Yes, they are. Of course, that’s also another rant for another day, and not our point right now.

Today, we’re less concerned with who the Fed is … and more focused on what they’re doing and what it REALLY means to Main Street real estate investors.

It’s a bit more complicated than just interest rates and inflation. Sorry. But it’s important because what’s brewing isn’t your run-of-the-mill financial crisis.

Back to our story …

So the Fed prints money from nothing and lends it to Uncle Sam. But when the government borrows money, who pays it back … and how?

Hint: The Federal Reserve, the income tax, and the IRS were all created at the same time as part of the 16th amendment in 1913.

Why?

Well, it seems there was a financial crisis in 1907, and the politicians and their funders decided to “fix” the situation.

Of course, “fix” is a word subject to interpretation …

“Repair, mend” … OR … “to influence the actions, outcome, or effect by improper or illegal methods”.

– Merriam-Webster Dictionary

And since we’re quoting …

“Never let a crisis go to waste.”

– Saul Alinsky

“Never let a good crisis go to waste.”

– Winston Churchill

“You never let a serious crisis go to waste. And what I mean by that it’s an opportunity to do things you think you could not do before.”

– Rahm Emanuel

You get the idea. Exploitation of a crisis is a standard operating political principle that’s been around a long time. And the consequences often land on Main Street.

And speaking of principles that have been around a long time …

“The rich rules over the poor; and the borrower is servant to the lender.”

Proverbs 22:7

Interesting.

We’re guessing you’re smart enough to put all that together for yourself. Must be nice to print money out of thin air and buy up trillions in debt.

Meanwhile, back on Main Street …

You don’t need to be a rocket surgeon to know you can only extract so much tribute … even at zero interest … before the burden is simply too much.

As we noticed last September, there were signs of severe systemic stress BEFORE the COVID-19 crisis hit.

Now everything is moving much faster … so it’s important to pay close attention and be ready to react to both the approaching dangers and opportunities.

Obviously, dollars are nearly free right now. It’s probably not a bad idea to grab all you can while credit markets are still functioning.

We’re noticing small businesses and commercial properties coming on the market at an increased pace … and with “price reduced!” in the pitch.

That’s a clue the crisis sale might be starting.

You also may have noticed precious metals are catching a bid in dollar terms. That’s talking head jargon for gold and silver prices are going UP on dollar price.

This indicates more dollar-denominated investors are choosing to keep some liquidity in precious metals versus currency.

This makes sense as every other currency in the world is already at all-time lows versus gold (i.e., gold is at all-time highs in every currency except the dollar).

When the Fed is printing trillions of dollars each year … and Uncle Sam is aggressively putting them into circulation … the historical result is a falling dollar.

And despite what you may hear on financial TV … we think it can be strongly argued this is setting up a perfect storm for leveraged income-producing real estate.

Remember, Wall Street and the TV gurus who promote them believe investing is “buy low, sell high”.

But real estate investors think “cash flow” … which is the only reliable source of equity. Income creates real equity.

Meanwhile, strategic real asset investors put it all together into a bigger picture …

Real estate (especially residential) is a sector strongly supported by the most powerful constituencies … politicians, bankers, and voters.

That’s a lot of love … and a great place in line when emergency help is doled out.

More importantly, debt is the real investment.

Income property mortgages are essentially a big short of the dollar with a great feature: the income from the property makes the payments.

So while you may not be able to print money like the Fed, using the right real estate debt is pretty close. And …

… the Fed is ALWAYS working on making debtors winners.

And when you use debt to convert real estate equity into precious metals, you have a very powerful shield against a falling dollar.

Yes, it’s true the dollar is catching the “best last paper currency standing bid” …

… but the dollar’s relative strength against other paper currencies at the same time it’s showing weakness against gold …

… is a major clue there’s some real-world weakness likely coming for the dollar in the not-too-distant future.

Yes, we know this is a lot to absorb. It’s why we keep repeating ourselves.

But rather than getting bored, we hope you’re getting inspired to study and prepare. This is a whole new ballgame.

This four-phase cascading crisis is still very early in its life-cycle.

It’s not the time to succumb to a short attention span.